Payment Service and Payment System

The terms “payment service” and “payment system" are generally used interchangeably to refer to the same meaning in banking practices. However, they are actually different terms as explained below.

Payment service includes services provided to users (customers) and transactions related to fund transfers realized with or without payment accounts within the payment service provider itself or in another payment service provider. Operation of payment accounts (e.g. cash deposits or withdrawals), issuance or acceptance of payment instruments (e.g. debit cards) and services related to mobile payments (direct carrier billing services), money remittance or bill payments as well as payment initiation services and account information services fall into this context.

For example, when a customer sends money from his/her bank account to another bank account, all kinds of services that the banks provide during this process are in the scope of payment services. In this case, the banks are the payment service providers and the customer is the beneficiary of the service. The payment system, on the other hand, refers to the special infrastructure used for interbank money transfers.

In Türkiye, interbank transfers are performed through a payment system called the Electronic Fund Transfer (EFT) System and operated by the CBRT. This system allows for a safe and fast transfer of funds between customers of different banks and interbank transactions.

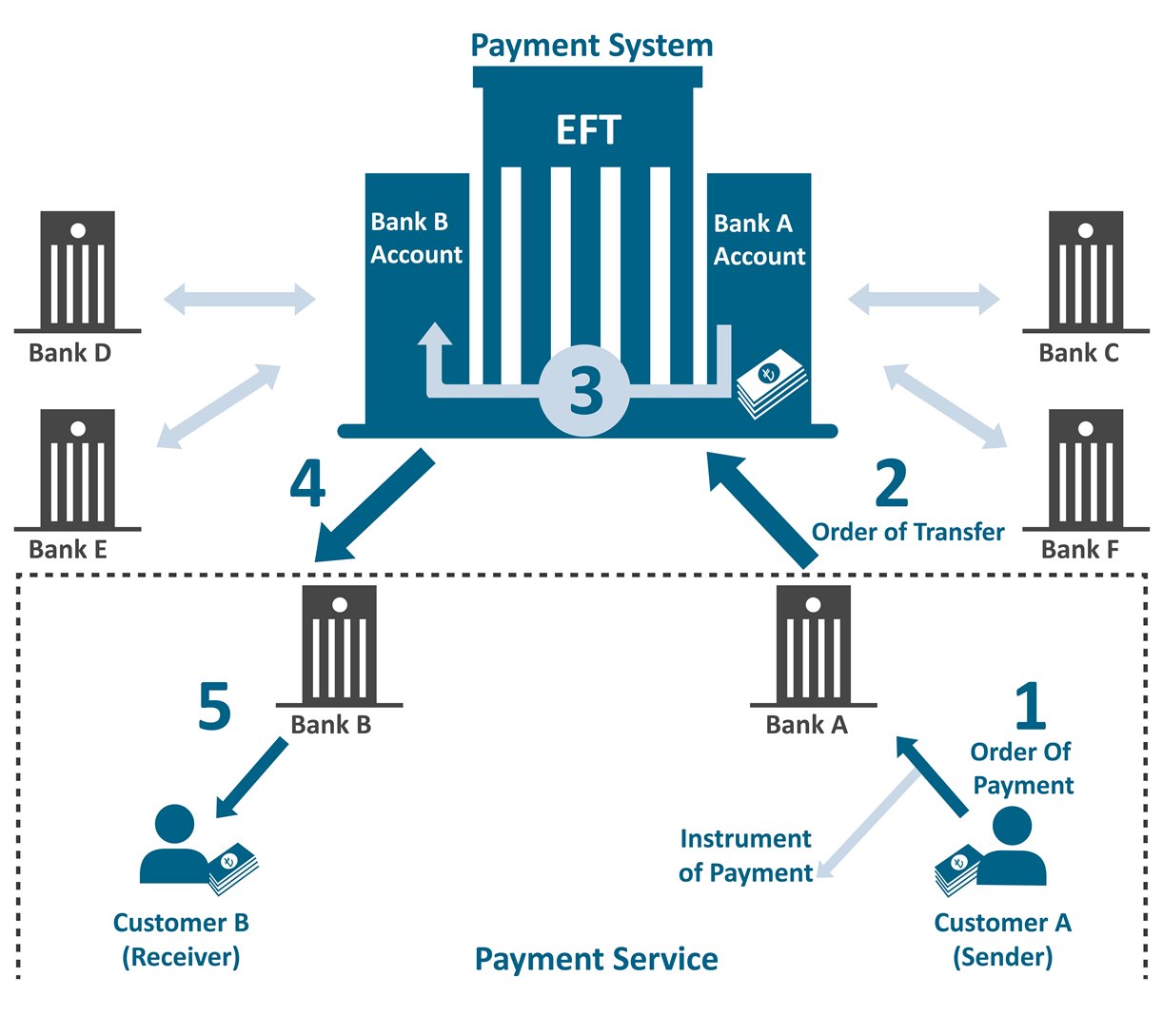

The working principle of the payment system

- Customer who is willing to send money, gives a payment instruction to his/her bank, which is a member (participant) of the system.

- The bank, after receiving the payment instruction from its customer, transmits this payment instruction to the system as a “transfer order”.

- The money is transferred from sender bank’s account to receiver bank’s account electronically via EFT System. The receiver bank is informed of the status of the transaction.

- The receiver bank is informed about the transaction.

- The receiver bank pays the money to the payee (its customer) according to the information received from the system.

Payment instruments used in this flow are personalized instruments such as cards, mobile phones, and passwords agreed upon by the payment service provider and the payment service user.

Actors in today’s economic world make payment transactions for various reasons. Institutions that are members of this system can carry out any payment transaction with each other by connecting the payment system.

Payment systems enable many complex interbank money transfer operations to be performed in a flawless and fast manner.

The following two concepts regarding the operation of payment systems are crucial:

Clearing: It is defined as transactions for transmission of transfer orders sent to the system, mutual communication of these orders, intermediation of the process of getting provisions, and in some cases, netting of orders.

Settlement: It is defined as fulfilling the liabilities arising from the transfer of funds or securities between two or more parties.

Accordingly, in the structure mentioned above, Step 2 and Step 4 are clearing transactions and Step 3 is settlement transactions. Step 1 and Step 5 are the transactions related to the payment services between banks and their customers.