Consumer inflation ended the year 2025 at 30.9%. While goods inflation was 25% over this period, services inflation remained high at 44%. In this post, we investigate the services sub-items that recorded the largest price increases in the consumer price index (CPI) basket in 2025, and explore the reasons for the relatively high levels of inflation in these items.

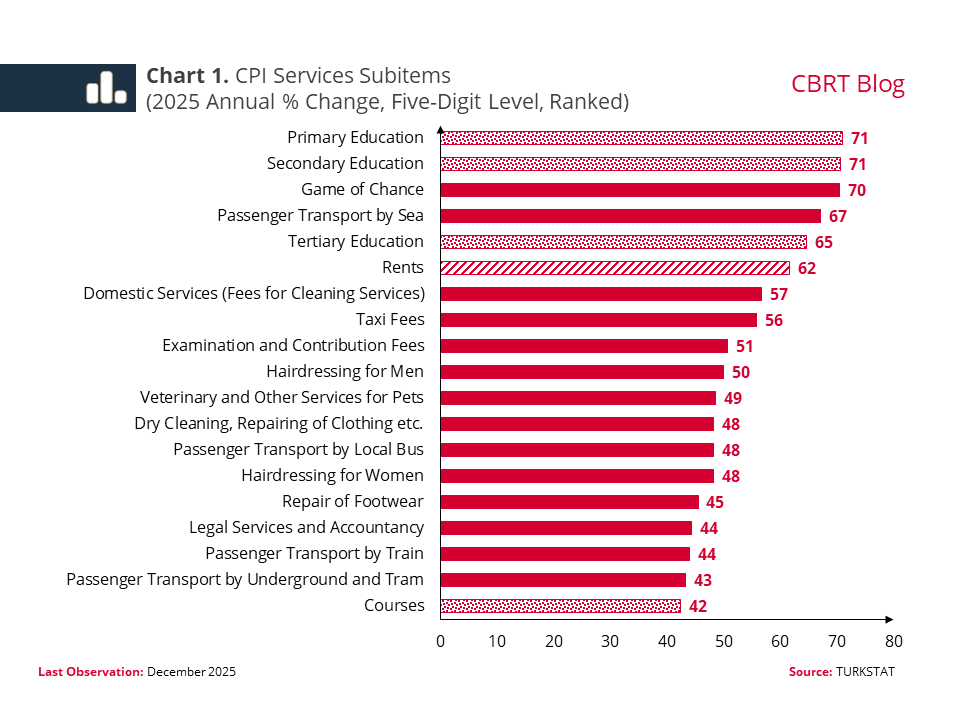

A ranking of price indices at the five-digit level based on their increase in 2025 reveals that 19 out of the first 30 items are services items. Three groups stand out among these: (i) education, (ii) rents, and (iii) locally provided services items with relatively limited competition (Chart 1).

(i) Education Services

Education services rank first among the items that posted the largest increase in 2025. From a longer-term perspective, since the end of 2019, consumer prices rose approximately eightfold while education services prices increased tenfold. It is notable that tertiary education fees ranked fourth among the sub-items that registered the highest rates of increase, with a 15.1-fold rise over this period.

One important factor in education inflation was the backward indexation stemming from existing regulation. Until recently, the regulation governing the pricing of private education was based on the 12-month average of consumer and domestic producer price increases. In practice, this amounted to using the past 24 months of inflation, thereby inducing substantial inertia. The amendment of September 5, 2025, effectively reduced backward indexation by limiting the maximum price increase in the current year to year end inflation in the previous year.

Under the former regulation, it took longer for an inflationary episode, to be reflected in education prices. Institutions that failed to rapidly adjust their prices during inflationary periods found themselves at a disadvantage. On the other hand, even when the impact of the shocks softened, the pace of disinflation remained slow as price adjustments were indexed to high inflation reflecting the impact of the previous 24 months. The latest amendment to the regulation may therefore be interpreted as a measure that will contribute to the disinflation process by relatively weakening the backward indexation mechanism.

(ii) Rents

Another item that stands out in the high course of services inflation is rents. Housing sector-specific factors, such as earthquakes, urban transformation, demographics, rent cap, and the fact that contracts are mostly renewed once a year with backward indexation, are increasing the inertia of rent inflation.

The transmission of monetary policy to the housing market may be lagged under these circumstances. Given that the impact of supply-side policies (e.g. urban transformation, social housing projects, etc.) is felt in the medium to long term, rent inflation will slow down but may remain higher than other service items for some time.

Moreover, the effect of services such as rents and education on inflation is not just confined to their direct impact arising from their consumption share. Pricing behavior in these sectors also has the potential to have secondary effects on inflation through the household budgets. Employers and the self-employed may take into account increases in the related payments in their own budgets when determining the prices of their products or services, while employees may demand higher wages.

(iii) Locally Provided Services with Limited Competitiveness

The third group consists of locally provided services items with relatively limited competitiveness (such as barbers/hairdressers, household cleaning services, veterinary services, dry cleaning, and footwear repair, etc.), as well as transport-related administered items (including ferry fares, taxis, urban passenger transport by local bus, and passenger transport by railway).[1] These transportation items share the characteristic of being locally provided, and their pricing process is shaped through administrative or semi-administrative decisions taken by local authorities.

Many of these services are labor-intensive, with prices directly constitute the income of the individuals providing the service. Accordingly, for those operating in these services, efforts to compensate for the erosion in purchasing power and their income and inflation expectations are important. As the service capacity offered per unit of time in these services is limited, it is often difficult to reduce unit costs through automation or increase in productivity. These services are provided at the province/district/neighborhood level and can sometimes be based on personal relations (such as neighborhood barber). In areas such as urban transportation services, consumer demand can continue despite price increases. In such local services, price competition can remain low, partly due to consumers' limited substitution options. These factors increase the pricing power of service providers, causing service inflation to follow a more persistent course compared to goods inflation.

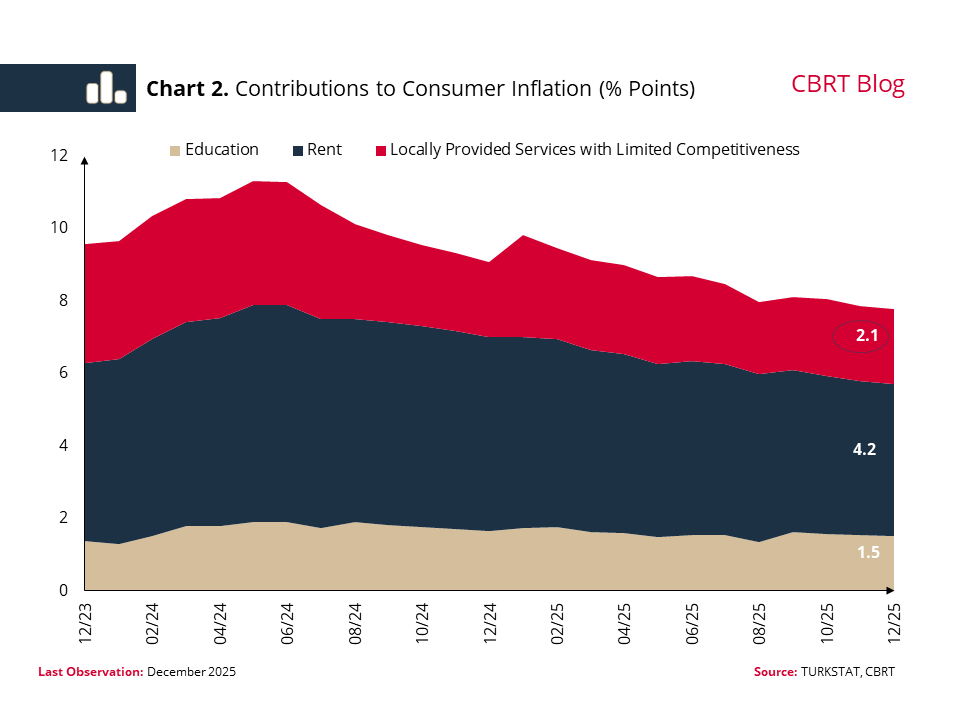

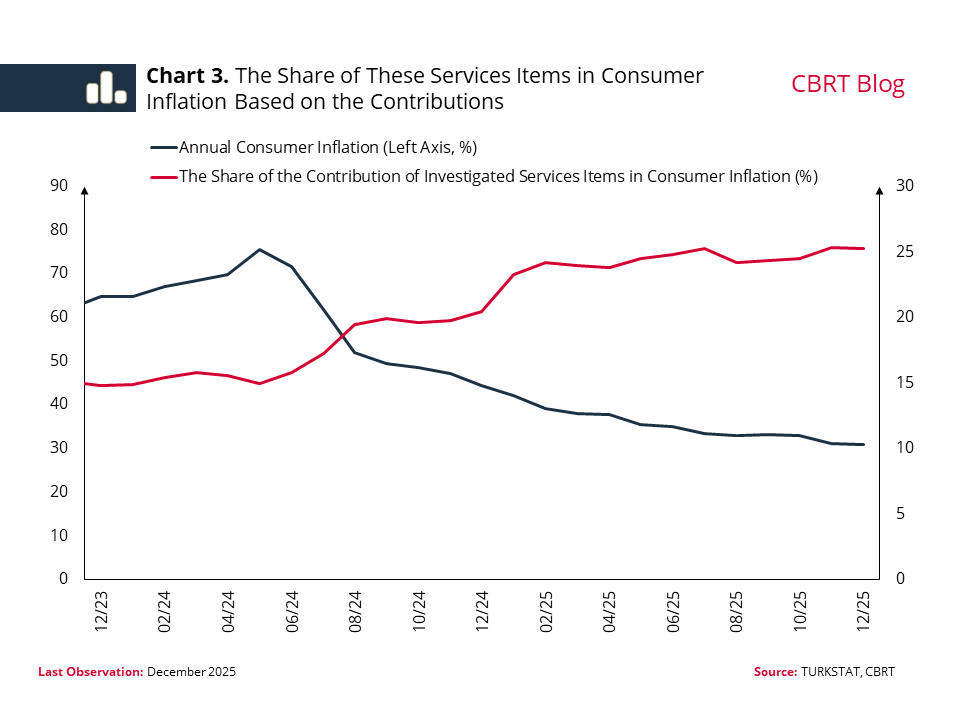

In the following section, we calculate the contribution of the aforementioned service items to consumer inflation. The contribution of these three groups to consumer inflation peaked at 11.3 percentage points in the May–June 2024 period (Chart 2). Although the contribution declined to 7.8 percentage points by the end of 2025, it remains high. By the end of the year, the contribution of rents, education, and locally provided and relatively less competitive services items to inflation was 4.2, 1.5, and 2.1 percentage points, respectively. The services investigated account for approximately a quarter of consumer inflation (Chart 3). Moreover, despite the decline in consumer inflation, the contribution of these three groups to inflation remained high throughout 2025, leading to significant inertia in the disinflation process. In 2025, the contributions of locally provided and relatively less competitive services items to inflation remained unchanged. Indeed, rent and education inflation declined by 44 and 25 percentage points, respectively, while the fall in inflation of local/relatively less competitive services items was limited to 2 percentage points.

To conclude, the education, rents and locally provided services items with limited competitiveness stand out as the key sub-items in the high course of service inflation in 2025. We expect that the latest regulatory change in education will contribute to the disinflation process by relatively weakening the backward indexation mechanism. On the rents front, both the seasonally adjusted price data and leading indicators for rents point to a downward underlying inflation. However, price increases in locally provided services items with limited competitiveness such as urban transport, barbers/hairdressers, household cleaning and dry cleaning may involve rigidities that can be attributed to income expectations, market structure, and pricing behavior, in addition to cost and demand factors. These rigidities are among the factors that affect the course of inflation and challenge the disinflation process.

[1] The fact that transportation-related items are at the top of the list initially suggests the impact of fuel costs. However, the 21.5% increase in fuel prices in 2025 indicates that factors other than the cost channel may also play a role.