Governor Başçı's Speech in Press Conference for the Presentation of the Inflation Report-III (Ankara, 26/07/2012)

Distinguished Guests,

Welcome to the press conference held to convey the main messages of the July 2012 Inflation Report. I will now present an overview of the third inflation report of 2012 that will be posted on our website shortly.

The Report typically summarizes the economic outlook underlying monetary policy decisions, shares our evaluations on macroeconomic developments and presents our medium-term inflation forecasts that have been revised in view of the developments in the past three months, along with our monetary policy stance. Moreover, the Report contains eight boxes entailing interesting and upto-date analyses on various topics. For instance, one of the boxes analyzes Turkey’s export performance related to product and country group diversification. There is another box evaluating economic activity in the second quarter from different perspectives. There is also a study exploring Turkey’s net foreign exchange position differentiating between the long and short term. You can see the titles of these eight boxes on the slide right now. The Report will be published on our website shortly and I recommend that you read these studies.

Now, I would like to summarize the main parts of the Inflation Report. Developments pertaining to global economic outlook continue to play an important role in our monetary policy decisions. Therefore, I would like to start with a brief evaluation of global economic outlook.

Developments in the Euro area have continued to shape the global economic outlook in the second quarter of 2012. Since the publication of the April Inflation Report, there have been major events in the Euro area affecting risk perceptions. Greek election results in May reduced the probability of an exit from the monetary union and rendered a partial recovery in risk perceptions. The measures taken accompanied by the supporting statements by leading central banks induced an improvement in global risk perceptions as of June. Nevertheless, further deepening of the interlinked problems in Spain with regards sovereign debt and banking sector has negatively affected the improvement in risk appetite. All these problems regarding the Euro area remain as a major risk for the global economy in the medium and long term.

The instability in the global economy coupled with ongoing imbalances continues to affect the global economic outlook adversely. In fact, in the past quarter, economic activity lost momentum over the globe including the U.S. and China. Accordingly, growth forecasts for advanced and emerging economies are also being revised downwards. While inflationary risks have waned in tandem with the weak outlook for global economic activity, concerns over growth and financial stability persist. Against this backdrop, central banks continue to implement expansionary monetary policies.

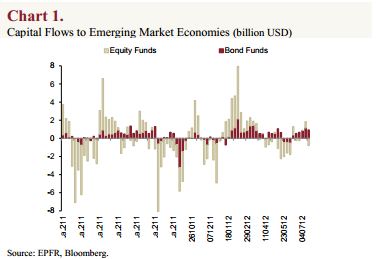

Continued fragilities and imbalances regarding the global economy cause the risk appetite to be highly volatile. Although it has been four years since the outbreak of the global crisis, economic units are still going through deleveraging. Problems in the Euro area, uncertainties regarding the U.S. and Chinese economies, as well as supply-side risks on energy prices persist. This, coupled with the extraordinarily low cost liquidity facilities provided by central banks, brings about considerable volatility in short-term capital flows to emerging economies (Chart 1). Such an environment urges central banks of emerging economies to give priority to measures aimed at containing the adverse effects of excessive volatility in short term capital flows. All these confirm the importance of having a flexible monetary policy framework.

1. Monetary Policy and Monetary Conditions

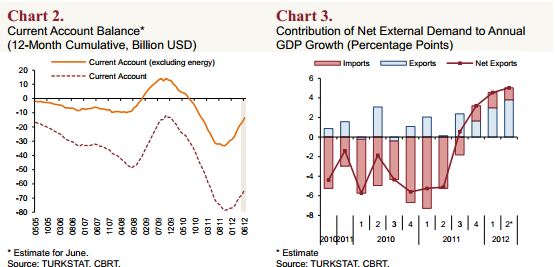

As of late-2010, the Central Bank of the Republic of Turkey (CBRT) has implemented a new policy aimed at managing macro financial risks in the shortterm, without prejudice to price stability in the medium-term. To this end, credit growth was brought under control and exchange rate was aligned closer with economic fundamentals. Data released for the first half of the year has shown that the policies pursued were considerably successful in delivering the intended results. The composition of growth displayed a healthier outlook, while the rebalancing process in the economy became more evident. In fact, during this period, current account balance continued to improve (Chart 2) and the contribution of net exports to growth increased markedly (Chart 3).

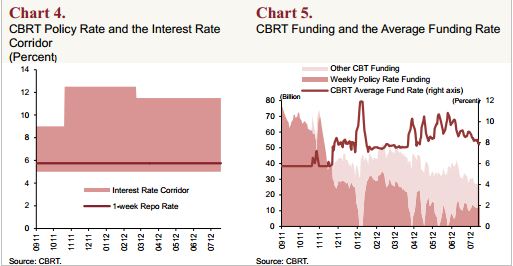

Once we started to attain the desired outcomes in reducing macro financial risks, we could focus on price stability, as of October 2011. In this respect, the CBRT implemented a strong monetary tightening by widening the interest rate corridor upwards and using liquidity operations effectively (Chart 4). As a consequence, the average funding rate has been above the policy rate then onwards (Chart 5).

In line with the periodic improvement in global risk appetite, the Monetary Policy Committee (the Committee) kept short-term interest rates almost unchanged in the early months of the year. Additional monetary tightening was implemented in April and May with an aim to contain the adverse effects of temporary factors on inflation outlook and to limit the risks regarding pricing behavior. This not only helped contain credit growth but also reduced inflation uncertainty by curbing exchange rate volatility. These policies proved to be quite effective in preventing a possible deterioration in inflation expectations, amid a period of intensified supply side pressures and double-digit inflation (Chart 6 and 7). Those, who wish to see a more comprehensive analysis on this issue, can read the economic note on the topic that was recently posted on our website.

I would like to continue summarizing the policies we have recently been implementing. The resurge in capital flows to emerging markets and the sharp fall in commodity prices, taking place both in June, reduced inflation risks. Moreover, risk perceptions for Turkey have improved on the back of the betterthan-expected inflation and current account data. Consequently, the CBRT has gradually reduced average funding rate since early June (Chart 5). Yet, the Committee preserved its cautious stance in its July meeting, highlighting the risks related to pricing behavior posed by inflation that will stay at high levels for some time. Moreover, the Committee stated that it would be appropriate to preserve the flexibility in monetary policy amid lingering uncertainties in the global economy. In this respect, we reiterated that the impact of the measures taken on credits, domestic demand, and inflation expectations would be closely monitored and, when necessary, the amount of Turkish lira funding shall be adjusted in either direction.

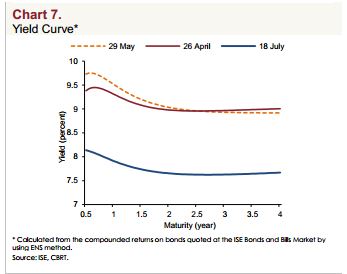

Now, I would like to briefly talk about how general monetary and financial conditions unfold within the framework of these policies. Yields on the market were gradually affected by the policies implemented. For instance, the yield curve became more negatively sloped in May, when frequent additional monetary tightening was implemented. With falling inflation expectations and declining risk premium, the yield curve shifted downwards in the post-June period (Chart 8).

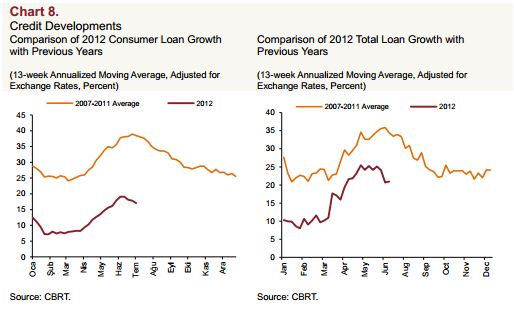

Meanwhile, credit conditions have been relatively tighter. The pick-up in credit growth in the second quarter can be attributed to seasonal factors rather than a permanent acceleration in credit growth. In this period, consumer credits grew at a much moderate rate compared to the average growth observed during the same periods of past years (Chart 8). Since the turn of the year, commercial credits have grown slightly more than consumer credits, reflecting a healthy composition. Credit growth is expected to follow a reasonable and healthy course in the forthcoming period, in line with the projection of a moderate increase in domestic demand.

2. Macroeconomic Developments and Main Assumptions

Now, I will touch upon the macroeconomic outlook and our assumptions that constitute the basis for our forecasts. First, I will compare the short-term forecasts in the April Inflation Report with realizations and summarize recent inflation developments. Then, I will briefly talk about domestic and external demand outlook.

In the second quarter of the year, inflation remained well below the forecasts given in the April Inflation Report and, owing to the better-than-projected course of oil and unprocessed food prices, declined to 8.9 percent by the end of June (Chart 9).

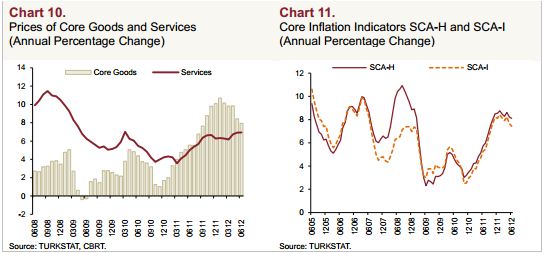

As the cumulative pass-through effect of exchange rate movements on domestic prices faded in 2011 confirming our assumptions, the core goods inflation continued to fall in annual terms. The prices of services slightly pickedup but followed a mild course (Chart 10). Against these developments, core inflation indicators maintained their downward trend (Chart 11).

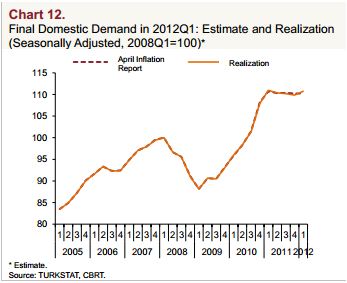

Now, I would like to summarize the outlook for economic activity. National accounts data for the first quarter of 2012 point that demand conditions have been broadly consistent with the outlook presented in the April Inflation Report (Chart 12). While final domestic demand remained weak, net exports’ positive contribution to annual growth accelerated (Chart 3).

Recently released data indicate that final domestic demand grew at a moderate rate, exports maintained an upward trend and the rebalancing in demand composition continued in the second quarter. Even if the economic activity is expected to post a relatively higher growth in the second quarter, this can be largely attributed to the low base at the initial months of the year, hence the recovery in economic activity is considered to be mild in this period.

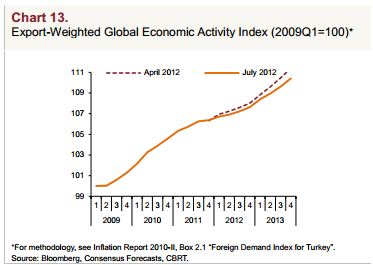

While producing our forecasts, we assumed that foreign demand would follow a weaker course in the second half of the year compared to the first half due to problems in the global economy, which would restrain aggregate demand. In fact, growth rates in both advanced and emerging economies were revised downwards in the past quarter (Chart 13). Although Turkey’s resilience against external shocks has been enhanced thanks to export partner and export product diversification in recent years, persistent weak growth outlook for the Euro area still poses a downside risk for external demand.

In sum, output gap forecasts for the first half of the year have remained broadly unchanged as domestic economic activity has been in line with the projections laid out in the previous report. As for the second half, the contribution of aggregate demand conditions to disinflation is assumed to be slightly higher compared to the previous reporting period owing to the weakening in the outlook for global economic activity. This update, due to its being quite limited did not have a significant effect on the inflation forecast for 2012.

As you know, food and energy prices also play important role in inflation forecasts. Therefore, before moving on to forecasts, I would like to briefly present you our assumptions regarding these variables.

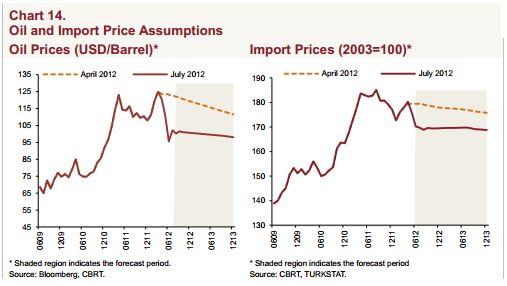

Oil prices remained below projections in the interreporting period (Chart14). Accordingly, taking into account the recent futures prices, the assumption for average oil price was reduced from USD 120 to USD 110 for 2012; and from USD 115 to USD 100 for 2013. In line with the overall fall in the prices of commodities, projections for import prices were also revised downwards (Chart 14). Considering the mentioned factors along with exchange rate movements, the combined effect of external price developments on the inflation forecast for end-2012 became 0.15 percentage points on the downside.

There was a limited downward revision in the assumption for food price inflation for end-2012. Due to the favorable course of unprocessed food prices in the first half of the year, food prices increased at considerably lower rates compared to historical averages. However, the overall effect of these lower rates was not reflected on our forecasts. Instead, forecasts were based on a cautious stance, which entailed the assumption that the favorable course of food prices in the first half would be largely reversed in the second half. Accordingly, the assumption for the annual rate of increase in food prices, which was 7.5 percent in the previous report, was revised downwards by only 0.5 percentage points to 7 percent in the current report. The contribution of this revision to the inflation forecast for end-2012 was around 0.15 percentage points on the downside.

Before moving on to forecasts, I would like to finally share with you our assumptions regarding the public finance. As usual, we base our assumptions on the revised projections of the Medium Term Program (MTP). Accordingly, the ratio of primary expenditures (accumulated over 12-months) to GDP is assumed to remain largely unchanged in the second half of the year. As per the arrangements introduced to taxes imposed on tobacco products in the last quarter of 2011, tobacco prices are envisaged to remain unchanged throughout 2012, and increase at the beginning of 2013 at rates implied by the tax adjustments announced in October 2011. Furthermore, other tax adjustments and administered prices are assumed to be consistent with the inflation targets and the automatic pricing mechanisms.

3. Inflation and Monetary Policy Outlook

Distinguished Guests,

Now, I would like to present our inflation and output gap forecasts based on the outlook I have described so far. When forming our forecasts, we have assumed that monetary policy will maintain its cautious and flexible stance, and annual loan growth rate will be around 14 percent by the end of the year as in the previous report. Accordingly, inflation is expected to be between 5.3 and 7.1 percent (with a mid-point of 6.2 percent) at the end of 2012, and between 3.4 and 6.8 percent (with a mid-point of 5.1 percent) at the end of 2013. Inflation is expected to stabilize around 5 percent in the medium term (Chart 15).

Overall, the year-end inflation forecast is lowered by 0.3 percentage points to 6.2 percent mainly owing to the downward revisions in energy and food prices (Chart 15). Revised forecasts indicate that inflation will resume a downward trend following a slight increase in July. However, I would like to emphasize that we will see the significant decline in inflation in the last quarter of the year. We expect that the fall in inflation will become more evident in the last quarter of the year since the base effect stemming from tax adjustments in administered products and unprocessed food will be removed. As for the core inflation indicators, the downward trend is expected to continue in the rest of the year.

At this point, I would like to emphasize that any new data or information regarding the inflation outlook may lead to a change in the monetary policy stance. Therefore, assumptions regarding the monetary policy outlook underlying our inflation forecasts should not be perceived as a commitment on behalf of the CBRT.

4. Risks and Monetary Policy

In the last part of my speech, I would like to share our assessment of the risks on inflation outlook. As I have mentioned at the beginning of my speech, the lingering uncertainties regarding the global economy requires the maintenance of a flexible approach in monetary policy. The perception that leading central banks will keep interest rates at low levels for a prolonged period encourages the search for alternative yields. Meanwhile, despite the steps taken for the resolution of problems regarding the Euro area, risk appetite remains highly sensitive to news due to ongoing fragilities in the financial system, elevated levels of sovereign borrowing costs and weakening growth outlook. Therefore, it is highly likely that short-term capital inflows will continue to be volatile in the forthcoming period. I would like to emphasize again that, it is important to preserve the flexibility of monetary policy in either direction in these circumstances.

In current circumstances, many different risk scenarios may be developed on the global economy. Now I would like to touch upon some of them, which we consider important, and inform you about how the monetary policy might be shaped should these risks materialize.

A further weakening in global economic outlook may prompt central banks of developed economies to implement additional monetary easing in the period ahead. We think that such an event may feed into macro financial risks for emerging economies like Turkey. A resurge in short term capital inflows may slow down the rebalancing process within the Turkish economy through rapid credit growth and appreciation pressures on domestic currency. Should such a risk materialize, the CBRT may keep short-term rates at low levels while tightening through reserve requirements, including the mechanism it has developed for reserve requirements by increasing the coefficients, which define the amount of foreign exchange to be held per unit of Turkish lira reserve requirements.

It is also likely that problems in the Euro area may further intensify, given the ongoing deleveraging process in banking, household and public sector balance sheets and possible delays in the institutional mechanisms to resolve the related problems. Should such a risk materialize and lead to a new global turmoil, the immediate reaction could be to implement an active liquidity policy via the interest rate corridor; to be followed by measures to relieve the tension in the banking system through the use of reserve requirements as well as other liquidity instruments. At this point, I would like to underline that our existing rich policy tools as well as having a flexible monetary policy make it possible for us to promptly take the necessary measures to relieve the tension in the financial system during these periods.

In the meantime, aggregate demand and commodity prices may increase faster than expected, should the measures taken towards the solution of problems regarding the global economy are completed sooner and more decisively than envisaged. Materialization of such a risk would possibly require a tightening using all policy instruments, as it would mean increased pressures on the medium-term inflation outlook.

Distinguished Guests,

Uncertainty regarding the commodity prices might be cited as another risk for the forthcoming period. Although weak global outlook dampens the upside pressures on commodity prices, prevailing geopolitical and supply-side problems pose upside risks regarding energy prices in the short term. Moreover, the recent rapid increase in agricultural commodity prices pose risks regarding processed food prices. Should such risks materialize, the CBRT will not respond to temporary price movements, yet will not tolerate any permanent deterioration in expectations and pricing behavior.

Unprocessed food prices pose downside risks on the inflation outlook in 2012, as indicated in the April Inflation Report. We have adopted a rather cautious approach in the current report, assuming a reversal in the favorable trend observed during the first half of the year. End-year inflation may be lower than projected in the baseline scenario, should the unprocessed food prices display a more favorable course than expected.

Inflation will continue to stay above the target for some time, necessitating a cautious stance regarding pricing behavior. Although the monetary tightening implemented since last October and the moderate outlook of aggregate demand reduces the likelihood of second round effects, pricing behavior will be monitored closely in the forthcoming period.

Distinguished Guests,

The CBRT will continue to monitor fiscal policy developments closely while formulating its monetary policy. As I have already mentioned, the forecasts presented in the baseline scenario take the framework outlined in the Medium Term Program as given. In this respect, it is assumed that there will be no additional deterioration in the budget balance in the second half of the year as well as no unforeseen hikes in administered prices. A revision in the monetary policy stance may be considered, should the fiscal stance deviate significantly from this framework and have a consequent adverse effect on the medium-term inflation outlook.

I would like to highlight that maintaining the prudent fiscal policy implemented in recent years is crucial for preserving the resilience of our economy against existing global uncertainties. Strengthening the structural reform agenda that would ensure the sustainability of the fiscal discipline and reduce the saving deficit would support the relative improvement of Turkey’s sovereign risk, and thus facilitate price stability and financial stability in the medium term. This will also provide more flexibility for monetary policy and contribute to social welfare by keeping interest rates on long-term government securities at low levels. In this respect, steps towards implementation of the structural reforms envisaged by the Medium Term Program remain to be of utmost importance.

While concluding my remarks, I would like to thank all my colleagues, who contributed to the Report, primarily those at the Research and Monetary Policy Department as well as the members of the Monetary Policy Committee, and thank every one of you for your participation.