Governor Başçı's Speech in Press Conference for the Presentation of the Inflation Report-I (İstanbul, 31/01/2012)

Distinguished Guests,

Welcome to the press conference held to convey the main messages of the January 2012 Inflation Report. As required by our new communications policy, we will hold two of the four inflation report press conferences in Istanbul, all of which used to be held in Ankara before. I will now present an overview of the first inflation report of 2012, which will be published on our web-site shortly.

The Report summarizes the economic outlook underlying monetary policy decisions, shares our evaluations on macroeconomic developments and presents our medium-term inflation forecasts which have been revised in view of the developments in the last quarter, along with our monetary policy stance. Moreover, the Report includes eleven boxes which entail interesting and up-todate analyses on various topics. For instance, there is an analysis on the functioning of our recent liquidity management policy and its effects on financial markets. There is also a box exploring the sources of changes in inflation forecasts in the previous year, which is a topic included in the first inflation report every year. Another box examines the base effects that will play a major role in the course of inflation in 2012. Also, there is a box that scrutinizes the steps taken to solve the debt problem in the euro area, which points out to the role of structural problems such as the marked divergence in member countries’ competitiveness in hindering stable growth in the euro area. There is also a box exploring the rebalancing process in domestic and external demand thanks to the policies implemented last year. Titles of the boxes are shown on the slide. All of these boxes include important analyses. They will be published on our web-site shortly and I strongly recommend that you read them.

Considering the ongoing major role of the developments in the global economy on our policies, I would like to start with the global economic outlook.

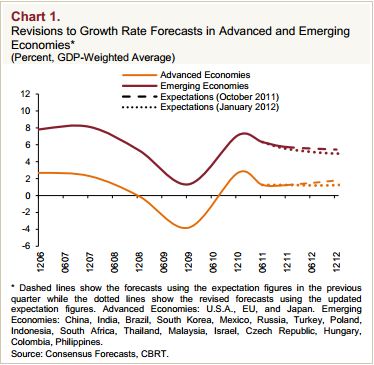

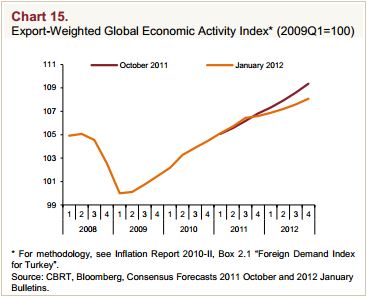

Since the publication of the October 2011 Inflation Report, concerns over sovereign debt sustainability across the euro area have continued to weigh on the global economic outlook despite the implementation of various policy measures. Growth forecasts were revised downwards at a global scale particularly in the euro area economies (Chart 1). Thus, perceptions for a further delay in the normalization of monetary policy in advanced economies grew stronger. Notwithstanding a relative improvement in the risk appetite as of the onset of 2012, uncertainties regarding the solution of euro area problems persist. Coupled with the increased risk of contagion, this feeds into the fragility in global financial markets, highlighting the significance of a flexible monetary policy framework.

1. Monetary Policy Developments and Monetary Conditions

The Central Bank of the Republic of Turkey (CBRT) has aimed at engineering the economy gradually towards a more balanced growth composition against the macro financial risks that aggravated in the first half of 2011. Accordingly, with the support of other institutions, necessary measures were taken to bring loan growth rates to reasonable levels. Furthermore, policies were geared towards preventing exchange rates from moving away from economic fundamentals excessively on either side (Charts 2 and 3).

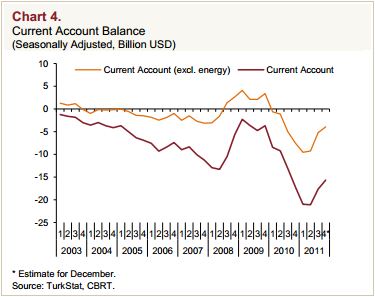

Data released for 2011 point that the desired rebalancing process in the economy has already started. Accordingly, the contribution of net exports to growth increased notably, and the current account balance posted a noteworthy improvement in the second half of the year (Chart 4).

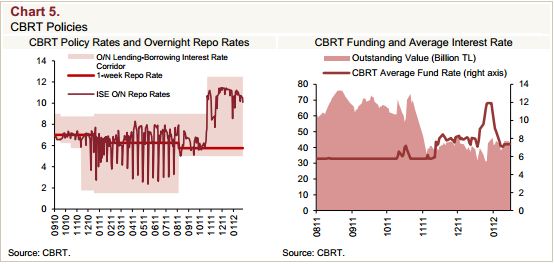

Despite the attainment of favorable outcomes regarding macro financial risks, soaring inflation in the last quarter required a revision of the monetary policy stance. The ongoing deterioration in the global risk appetite as of August led to an excessive depreciation in the Turkish lira posing risks on the inflation outlook. In addition, sizeable price adjustments in administered products in October led the short-term inflation to increase above forecasts. In order to not to allow inflation expectations to deteriorate, the CBRT delivered an important tightening in monetary policy since October. Accordingly, the interest rate corridor was widened upwards and the amount of the Turkish lira funding through one-week repo auctions was adjusted and the average funding cost was raised significantly (Chart 5).

The Monetary Policy Committee believes that the tight monetary policy stance should be maintained for a while to ensure that the inflation outlook is consistent with the medium term targets. Moreover, due to the ongoing uncertainties regarding the global economy, we are of the opinion that maintaining a flexible monetary policy will be appropriate.

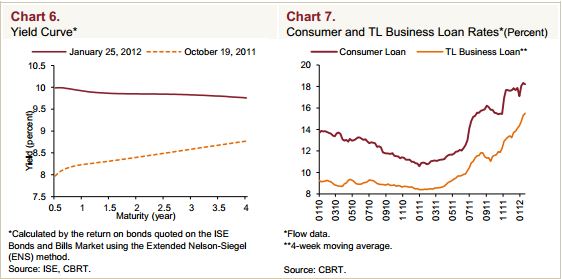

The downward slope of the current yield curve signifies a tight monetary policy stance (Chart 6). Additionally, loan interest rates have recorded a notable increase since October (Chart 7). As a consequence, loan growth rate declined to more reasonable levels towards the year-end (Chart 3).

Overall, the last quarter of 2011 was marked by ongoing tightening in monetary and financial conditions and a pronounced deceleration in loans.

2. Macroeconomic Developments and Main Assumptions

Having climbed to 10.45 percent at end-2011, inflation was significantly above the target. As you all know, the Article 42 of the Central Bank Law stipulates that in the case of a significant breach of the inflation target, we are required to report to the Government and announce to the public the reasons behind the breach of the target and the necessary measures to be taken. I would like to announce that we will publish the Open Letter that will be sent to the Government today on our web-site at 12 a.m.

Now, I will touch upon the macroeconomic outlook and our assumptions which constitute the basis for our forecasts. First, I will summarize the recent inflation developments, and then compare the short term forecasts in the October Inflation Report with the actual inflation data regarding the fourth quarter of 2011.

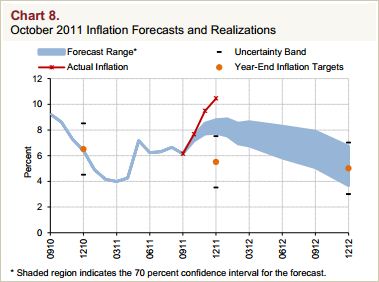

There were a few developments in the interreporting period which led inflation to deviate significantly from October forecasts. More-than-envisaged increases in unprocessed food prices were an important cause of this deviation. The ongoing depreciation in the Turkish lira amid the deterioration in the risk appetite was another factor leading to a deviation in short-term forecasts (Chart 8).

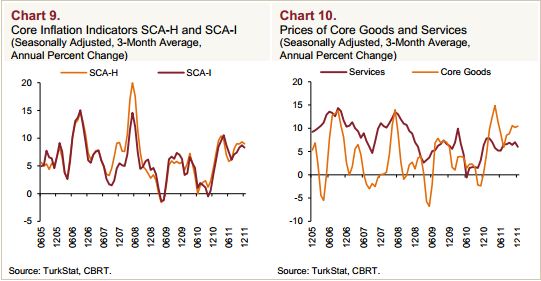

Owing to the lagged effects of the exchange rate pass-through, core inflation indicators remained at elevated levels during the final quarter (Chart 9). This mainly stemmed from soaring core goods prices, while the moderate course of the underlying trend of services inflation indicated a benign outlook in terms of second round effects (Chart 10).

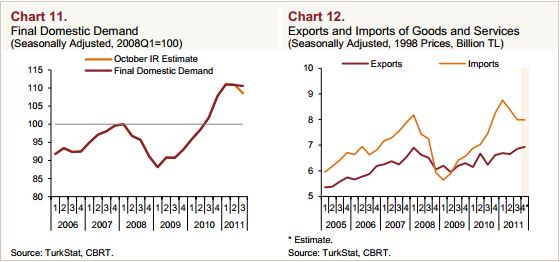

We see that economic activity remained robust in the second half of 2011, despite a slight deceleration. Gross Domestic Product (GDP) data pointed that domestic demand proved stronger in the third quarter of 2011 compared to the outlook presented in the October Inflation Report (Chart 11). Thus, we revised our output gap forecasts for this period upwards. Growth composition became much more balanced as we expected (Chart 12). Despite the weak course of the global economy, exports continued to increase, whereas the demand for imported goods and services maintained a downward trend. Consequently, the contribution of net external demand to growth has been positive for the first time after a protracted period.

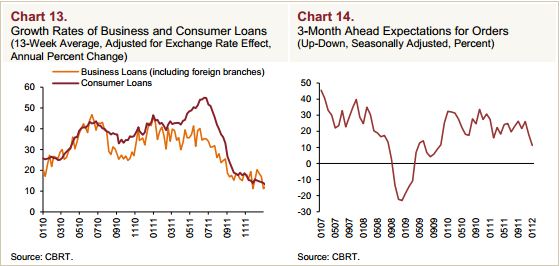

Indicators regarding the last quarter of 2011 point that final domestic demand remains flat and the rebalancing process in the economy is going on as envisaged. Owing to the monetary tightening, the growth rate of final domestic demand is expected to remain moderate in the forthcoming period, as suggested by the recent loan and orders data (Chart 13). Accordingly, our inflation forecasts are based on the assumption that domestic demand will decelerate further during early 2012.

In sum, we revised our output gap forecasts upwards for the second half of 2011 considering the stronger-than-expected economic activity in the third quarter. Meanwhile, due to the deterioration in the global growth outlook, we estimate that aggregate demand conditions will provide a stronger support to disinflation in the medium term compared to the previous reporting period.

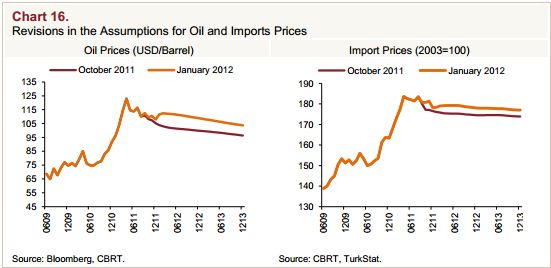

We also revised our assumptions for commodity and oil prices slightly upwards. Considering the recent developments and futures prices, we revised our assumptions for oil prices upwards from USD 100 to USD 110 per barrel for 2012 and to USD 105 for 2013. Accordingly, our assumptions for import prices were also subject to a slight upward revision (Chart 16). In addition, we preserved our assumptions for the annual rate of increase in food prices at 7.5 percent throughout the forecast horizon.

3. Inflation and Monetary Policy Outlook

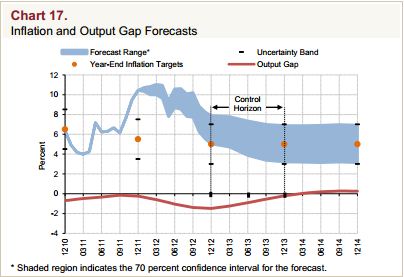

Now, I would like to present our inflation and output gap forecasts based on the outlook I have described so far. When forming our forecasts, we assumed that the tight monetary policy stance will be sustained for a while; and consequently, annualized loan growth rate will hover around 15 percent and the Turkish lira will display a mild appreciation trend. Accordingly, inflation is expected to be, with 70 percent probability, between 5.1 and 7.9 percent with a mid-point of 6.5 percent at the end of 2012, and between 3.3 and 6.9 percent with a mid-point of 5.1 percent at the end of 2013. We expect inflation to stabilize around 5 percent in the medium term (Chart 17).

Overall, although demand and cost conditions have not changed notably since the publication of the October Report, we revised our inflation forecasts for end- 2012 upwards due to higher initial point (the initial point referring to the latest inflation data before the forecast period) resulting from higher-than-expected inflation during the past three months.

As elaborated on in the Report as well, cumulative increases in the exchange rate and commodity prices coupled with soaring unprocessed food prices and the developments in administered prices pushed inflation to high levels in 2011. We estimate that inflation will remain flat in the first quarter and exhibit a gradual downtrend starting from the second quarter (Chart 17). Our tight monetary policy stance since October prevents a deterioration in the price setting behavior by keeping inflation expectations under control. Thus, we expect that inflation will follow a downward trend as the accumulated effects of the temporary price movements on annual inflation gradually fade away. Thus, we estimate that inflation will display a notable decline particularly in the last quarter of 2012.

Before moving on to the risks regarding the inflation outlook, there is a particular subject I would like to touch upon. As you might have noticed, I have given an inflation forecast that exceeds our end-year inflation target of 5 percent. This is because we think that pulling inflation towards the target by end-2012 would prove to be quite costly. Reducing inflation from the current level of 10.45 percent to 5-percent-target within 12 months would lead to unfavorable fluctuations in economic activity; accordingly we think that it is more reasonable to bring inflation back to the target in one and a half year. Thus, our baseline scenario envisages inflation to reach the target of 5 percent by mid-2013 (Chart 17). However, the target might be attained by the end of 2012, should the risk appetite improve markedly in the forthcoming period and the capital flows towards emerging economies re-accelerate, leading to a stronger appreciation of the Turkish lira than assumed in our baseline scenario.

At this point, I would like to emphasize that any new data or information regarding the inflation outlook may lead to a change in the monetary policy stance. Therefore, assumptions regarding the monetary policy outlook underlying our inflation forecasts should not be perceived as a commitment on behalf of the CBRT.

4. Risks and Monetary Policy

In the last part of my speech, I would like to share our assessment of the risks on inflation outlook. The first of these risks is the possibility of second round effects that might stem from inflation hovering at high levels in the short term. Three-month accumulated increase in consumer prices in the final quarter of 2011 was 5.66 percent. This will stay in annual inflation figure for another three quarters. Therefore, it is highly likely that annual inflation will stay significantly above the target until the last quarter of the year, even if the underlying trend in the forthcoming period eases to levels consistent with the target. Although the monetary tightening delivered by the CBRT since October has reduced the possibility of second round effects, I would like to emphasize that inflation expectations and pricing behavior will be monitored closely and necessary measures will be taken to keep medium-term inflation outlook consistent with the target.

Ongoing uncertainties regarding the global economy call for a continuation of a flexible approach in monetary policy. The medium term outlook presented in the Report assumes that problems in the euro area will be resolved gradually and the global outlook will not deteriorate further. However, the probability that the solution of the problems may take a more protracted and painful process poses downside risks regarding the global growth and risk appetite. On the other hand, perceptions regarding the global economic outlook may turn more favorable than expected, should the measures taken towards the solution are completed sooner and more decisively than envisaged. Such a situation, coupled with the ongoing quantitative easing policies pursued by the central banks of advanced economies, may improve risk appetite and re-accelerate capital flows towards emerging economies. Overall, ongoing problems in the euro area and uncertainties regarding the effectiveness of measures aimed at solving these problems suggest that global financial markets will continue to be volatile in the forthcoming period. These conditions necessitate a flexible approach in monetary policy, which utilizes multiple instruments. I would like to underline once more that the CBRT will continue to monitor global developments closely and take the required measures promptly.

Another risk on the inflation outlook is the uncertainty regarding oil prices. Although weak global outlook dampens commodity prices, rising problems of oil supply have recently posed upside risks on energy prices. I would like to reiterate that should such a risk materialize, the CBRT will not respond to temporary price movements, yet will not tolerate any deterioration in expectations.

We will continue to monitor fiscal policy developments closely while formulating monetary policy. In this respect, our baseline forecasts take the Medium Term Program as given and thus assume that fiscal discipline will be maintained. A revision in the monetary policy stance may be considered, should the fiscal stance deviate significantly from this framework and consequently have an adverse effect on the medium-term inflation outlook.

We will continue to focus on price stability in the formulation of the monetary policy while preserving financial stability as a supplementary objective. To this end, we will carefully assess the impact of the macroprudential measures taken by the CBRT and other institutions on the inflation outlook. We are of the opinion that strengthening the structural reform agenda that would ensure the sustainability of the fiscal discipline and reduce the saving deficit would support the relative improvement of Turkey’s sovereign risk, and thus facilitate price stability and financial stability in the medium term. This will also provide more flexibility for monetary policy and contribute to social welfare by keeping interest rates of long-term government securities at low levels. In this respect, I would like to end my remarks reminding you the importance of the steps towards implementation of the structural reforms envisaged by the Medium Term Program.

Thank you very much for your participation.