Governor Başçı's Speech in Press Conference for the Presentation of the Inflation Report-II (Ankara, 26/04/2012)

Distinguished Guests,

Welcome to the press conference held to convey the main messages of the Inflation Report. I would like to present you with an overview of the second inflation report of 2012, which will be published on our website shortly. As usual, the Report summarizes the economic outlook underlying monetary policy decisions, shares our evaluations on global and domestic macroeconomic developments and presents our monetary policy stance along with the medium-term inflation forecasts that have been revised in view of last quarter developments. In addition, the report includes ten boxes, each of which addresses captivating and up-to-date analyses on various topics. For example, there is an analysis on our communications policy and inflation expectations. Another box addresses potential differences that might be driven by different seasonal adjustment methods in evaluating the main trend of economic activity. The report also includes an analysis of the New Incentive System made public on April 5. It also contains a box that scrutinizes the rebalancing between domestic and foreign demand that started to be observed on the back of the policies implemented. Titles of the boxes are shown on the slide; all include important analyses; they will be published shortly on our website. I recommend that you read them.

Esteemed Guests,

I would now like to present a summary of the main parts of the Inflation Report. Global economic developments continue to play an important role for our policies. Therefore, I would first like to briefly mention about the global economic outlook.

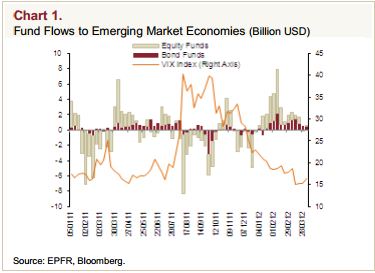

While global economic activity continued to slow down as expected in the first quarter of 2012, global risk appetite improved notably as concerns over the euro area eased. The prospect of a disorderly Greek default was averted with the completion of debt restructuring. This, along with the continued provision of three-year liquidity by the European Central Bank (ECB), resulted in a partial improvement in perceptions about the euro area debt crisis. Another factor that contributed to the air of confidence was the better-than-expected economic activity in the US. All these developments fuelled the global risk appetite and accelerated capital flows towards emerging economies in the first quarter of the year. More recently, however, bond yields have started to rise again due to increased concerns over the Spanish economy in particular. What is more, the rise in employment in the US fell short of expectations. Taken together, these developments interrupted the improvement in perceptions about the global economy. As a result, capital flows towards emerging economies became more volatile early on in the second quarter (Chart 1).

Developments since the January Inflation Report show that global financial markets remain fragile. Although it has been almost four years since the outbreak of the global crisis, the deleveraging process in advanced economies still continues. Problems about the euro area, uncertainties regarding the US and Chinese economies as well as supply-side risks on energy prices still persist. Even in periods of rapid rises in asset prices and the loose monetary policy stance in advanced economies, borrowing markets remain stagnant and concerns over the institutions that operate in these markets remain alive. All these developments suggest that the volatility in global risk perceptions may continue, confirming the importance of a flexible monetary policy framework.

1. Monetary Policy Practices and Monetary Conditions

Distinguished Guests,

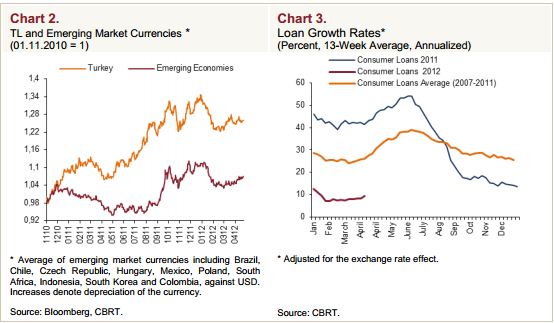

We have already stated that against the macro financial risks that intensified in the first half of 2011, the Central Bank of the Republic of Turkey (CBRT) aimed to steer the economy gradually towards a more balanced growth composition. Accordingly, necessary measures were taken with the support of other institutions to push loan growth rates down to reasonable levels. Moreover, policies were implemented to prevent excessive deviation of exchange rates from economic fundamentals in either direction (Chart 2 and Chart 3).

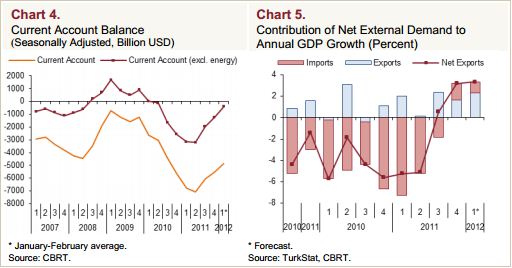

Data released since the publication of the January Inflation Report indicate that the rebalancing process in the economy continues as envisaged. There is a significant slowdown in growth rates of loans since the second half of 2011. Accordingly, the current account balance displayed a notable improvement (Chart 4). In this period, domestic demand growth was contained and the contribution of net exports increased markedly (Chart 5). In other words, growth composition assumed a healthier outlook.

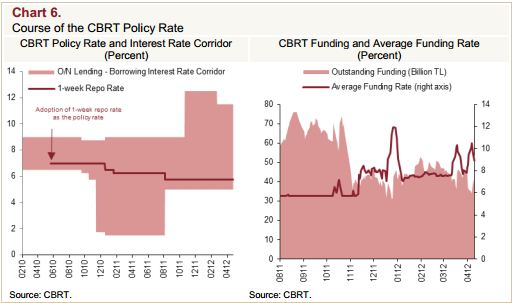

Having achieved the desired outcomes regarding macro financial risks, monetary policy focused on price stability as of October 2011. Cumulative effects of rises in import prices and the depreciation of the Turkish lira, tax adjustments in administered prices (tobacco and energy items) and hikes in unprocessed food prices led to a surge in inflation in the last quarter of the year. Although these developments are mostly temporary, the resulting high inflation brought about the risk of deterioration in inflation expectations. In this respect, in order to prevent a worsening in pricing behavior, the CBRT implemented a strong monetary tightening as of October by widening the interest rate corridor upwards and using liquidity operations efficiently (Chart 6).

Distinguished Guests,

Utilizing the flexibility offered by the interest rate corridor, additional monetary tightening has been implemented three times since October (Chart 6). During episodes of additional monetary tightening, the CBRT significantly raised the average cost of liquidity provided to the market by reducing the funding supplied through quantity auctions. On the other hand, the upper limit of the interest rate corridor was slightly lowered in February following the rise in the global risk appetite due to the improvement in perceptions regarding the euro area debt crisis (Chart 6). Yet the CBRT maintained its tight monetary policy stance. Accordingly, in April, the Monetary Policy Committee (the Committee) underlined that additional monetary tightening might be implemented more frequently in order to prevent a deterioration in the inflation outlook that may be driven by price adjustments in energy items and other temporary factors. In addition, the Committee stated that it would be appropriate to preserve flexibility in monetary policy as uncertainties regarding the global economy still persist.

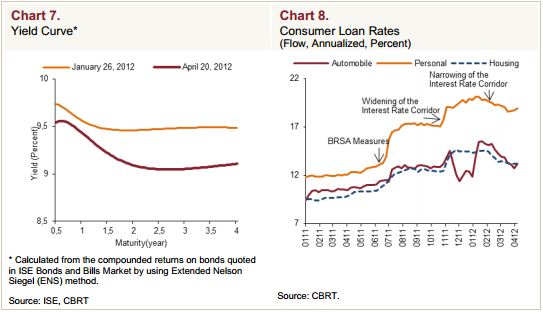

Keeping the interest rate corridor wide and implementing infrequent additional tightening results in a tight monetary policy stance. As a matter of fact, the downward slope of the yield curve as well as the slowdown in consumer loan growth rates and the relatively high interest rates on loans confirm that monetary and financial conditions are tight (Chart 7 and Chart 8).

2. Macroeconomic Developments and Assumptions

Esteemed Guests,

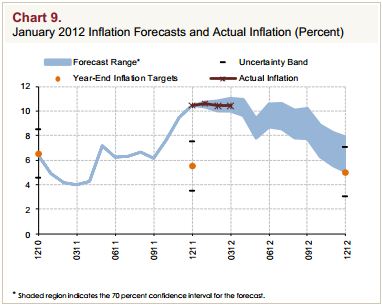

Now, I will touch upon the macroeconomic outlook and our assumptions, which constitute the basis for our forecasts. First, I will summarize recent inflation developments, and then compare short-term forecasts in the January Inflation Report with actual inflation data regarding the first quarter of 2012. In line with January Inflation Report projections, inflation became 10.43 percent by the end of the first quarter (Chart 9). In this period, oil prices were higher than assumed, which drove energy prices above projections. Meanwhile, unprocessed food prices followed a more favorable course than envisaged.

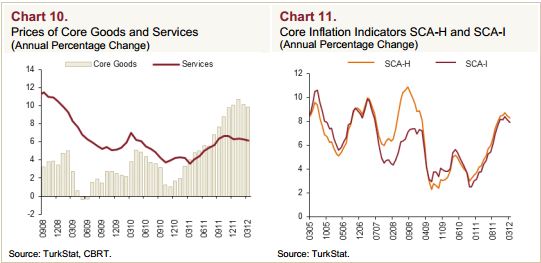

As the cumulative effects of exchange rate movements faded, the annual rate of increase in core goods prices trended downwards in the first quarter of the year. Meanwhile, prices of services maintained a mild course (Chart 10). Against these developments, core inflation indicators exhibited a downward trend after an extended period (Chart 11).

Distinguished Guests,

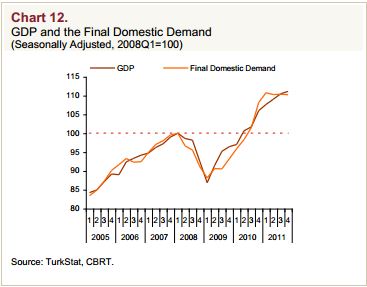

Now I would like to summarize the outlook regarding economic activity. National income data regarding the last quarter of 2011 indicate that aggregate demand conditions were broadly in line with the outlook presented in the January Inflation Report. Economic activity, which continued to decelerate due to weaker domestic demand, sustained its growth at a slower pace owing to the positive contribution of net exports (Chart 12).

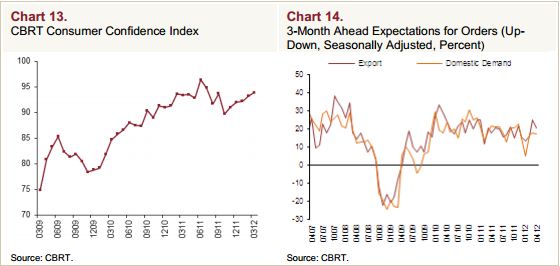

Industrial production data regarding early 2012 indicate that economic activity was slightly weaker than expected in the first quarter of the year. Nevertheless, this is considered to stem largely from temporary factors like unfavorable weather conditions and uncertainties regarding the global economy. Hence, a mild recovery is expected as of the second quarter. Indeed, the upward trend in indicators for orders and consumption goods for February and March signifies that the decline in economic activity is temporary (Chart 13 and Chart 14).

In the first quarter of the year, indicators for the global economy and external demand were also in line with expectations. Growth rates in both advanced and emerging economies continued to decline, while outlook remained weak especially for the euro area.

In sum, there has not been a major change in the outlook for domestic and external economic activity compared to the previous report period. Accordingly, as in the January Inflation Report, inflation forecasts are based on the assumption that the economy will revert to a mild growth path as of the second quarter and aggregate demand conditions will continue to support disinflation.

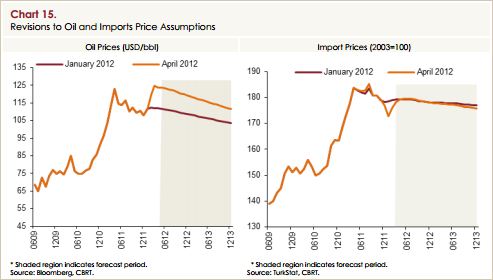

As is known, food prices, and oil and other imports prices play a crucial role in inflation forecasts. Therefore, before moving on with the forecasts, I would like to present our assumptions pertaining to the variables in question. The assumption for the annual rate of increase in food prices for end-year was maintained as 7.5 percent along the forecast horizon. Nevertheless, we revised our forecasts for oil prices upwards. Since the publication of the January Inflation Report, oil prices have remained significantly above the assumed path due to supply-side developments (Chart 15). Accordingly, taking also into account the futures prices in the first half of April, we revised our assumptions for oil prices upwards from USD 110 to USD 120 for 2012; and from USD 105 to USD 115 for 2013. Meanwhile, parallel to the decline in non-energy import prices, aggregate import price index displayed a better-than-expected course (Chart 15).

As a result, despite the better-than-expected prices in non-energy imports in the first quarter of the year, import prices slightly pulled up the inflation forecast for end-2012, due to the upward revision in energy prices, which have a stronger effect on the consumer price index. In the Report, there is a box examining the latest trends in imports prices in detail that I highly recommend you to read it.

Before moving on to the forecasts, I would like to briefly talk about our assumptions pertaining to public finance. As usual, assumptions for public finance are based on the outlook presented in the Medium Term Program (MTP). Therefore, the baseline scenario envisages that the ratio of primary expenditures to GDP will remain flat and the structural budget balance will not deteriorate. Moreover, tax reductions and other forms of state subsidies that will be enforced under the “new incentive system”, which was announced to the public on April 5, are assumed to cause no deterioration on the budget balance.

The baseline scenario envisages that tobacco prices will remain unchanged throughout 2012; but in January 2013, they are assumed to increase in tandem with the tax adjustments announced in October 2011. Other tax adjustments and administered prices are assumed to be consistent with the inflation targets and automatic pricing mechanisms.

3. Inflation and Monetary Policy Outlook

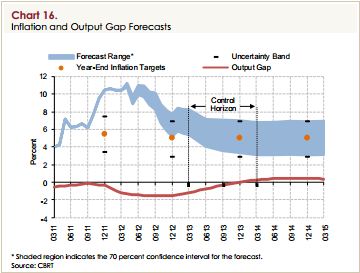

Now, I would like to present our inflation and output gap forecasts based on the outline given so far. When forming our forecasts, we assumed that additional monetary tightening would be implemented more frequently; and consequently, annual growth rate of loans would hover around 14 percent. Accordingly, inflation is expected to be, with 70 percent probability, between 5.3 and 7.7 percent (with a mid-point of 6.5 percent) at the end of 2012, and between 3.4 and 7.0 percent (with a mid-point of 5.2 percent) at the end of 2013. Inflation is expected to stabilize around 5 percent in the medium term (Chart 16).

Notwithstanding the unfavorable impact on inflation of the upward revision in the forecasts for energy prices in 2012, inflation forecast for end-2012 remained intact at 6.5 percent due to the offsetting impact of a tighter monetary policy stance. In this respect, the inflation forecast is based on the assumption that compared to the previous report period, credit growth will be more modest and aggregate demand conditions will now support the disinflation process more.

In the second quarter, inflation is expected to follow a volatile course due to temporary factors and base effects. In April, the direct effects of electricity and natural gas price hikes are expected to be around 0.5 percentage points and annual inflation is expected to increase temporarily and reach its peak. Due to base effects in unprocessed food prices, inflation is expected to display a sharp fall in May to be followed by a mild increase in June (Chart 16). It is expected that the tight monetary policy implemented by the CBRT since October 2011 will contain the second round effects, and thus inflation will follow a downward path once the cumulative impacts of temporary factors gradually taper off. Accordingly, it is envisaged that inflation would decline gradually as of the third quarter and the downward trend would become more evident during the final quarter of the year (Chart 16).

It should be once again underlined that any new data or information regarding the inflation outlook may lead to a change in the monetary policy stance. Therefore, assumptions regarding the monetary policy outlook underlying the forecasts should not be perceived as a commitment on behalf of the CBRT.

4. Risks and Monetary Policy

In the last part of my speech, I would like to share our assessments pertaining to the risks on inflation outlook. The existing high levels of inflation and the recent deterioration in short-term inflation expectations pose risks to the pricing behavior. Annual inflation is expected to hover significantly above the target until the final quarter of the year due to the sharp price increases witnessed during the last quarter of 2011. This urges us to keep a close eye on the pricing behavior. Although the monetary tightening implemented since October coupled with the moderate outlook of domestic demand have reduced the likelihood of the emergence of second round effects, the CBRT will adopt a cautious approach by monitoring inflation expectations closely, and will take necessary measures to keep medium-term inflation outlook consistent with the target.

Ongoing uncertainties regarding the global economy necessitate a flexible approach in monetary policy against potential volatilities in capital flows. Although sovereign debt problems in the euro area have alleviated somewhat during the first quarter of the year, bleak growth prospects and the still-high borrowing costs across the region keep debt sustainability debates alive. Moreover, the ongoing deleveraging process in the euro area banking system feeds into financial fragilities, increasing the probability of a renewed deterioration in the risk appetite. Meanwhile, the risk appetite may recover faster than expected, should the measures towards the solution of problems regarding the global economy are taken sooner and with more determination than expected. Overall, the possibility that global capital flows might continue to be volatile in the forthcoming period reaffirms the need for the current flexibility in the monetary policy framework. In this respect, the CBRT will continue to monitor global developments closely and take the required measures promptly.

Another risk for the forthcoming period is the uncertainty surrounding the outlook for oil prices. Although weak global economic outlook dampens the upside pressures on commodity prices, prevailing supply-side problems pose an upside risk to energy prices in the short term. I would like to reiterate that should such a risk materialize, the CBRT will not respond to temporary price movements, yet will not tolerate any permanent deterioration in the pricing behavior.

Meanwhile, unprocessed food prices pose a downside risk to inflation outlook in 2012. The probability of a downward correction in unprocessed food prices due to the high base attained by end-2011, coupled with favorable precipitation during recent months, increase the likelihood of a more favorable path for unprocessed food prices than those foreseen in our assumptions. Inflation may reach the target faster than projected in the baseline scenario, should the unprocessed food prices display a more positive course than expected.

The CBRT continues to monitor fiscal policy developments closely while formulating monetary policy. In this respect, the forecasts presented in the baseline scenario take the framework of the Medium Term Program as given and thus assume that fiscal discipline will be adhered to. A revision in the monetary policy stance may be considered, should the fiscal stance deviate significantly from this framework and have an adverse effect on the mediumterm inflation outlook.

Strengthening the structural reform agenda, which would ensure not only lasting fiscal discipline, but also lower savings deficit, would support the relative improvement in Turkey’s sovereign risk, and thus reinforce price stability and financial stability in the medium term. Steps taken to this end will also give monetary policy more room for maneuver and contribute to social welfare by keeping interest rates of long-term government securities at low levels. In this respect, efforts towards implementation of the structural reforms envisaged in the Medium Term Program remain to be of utmost importance.

I would like to thank all the Central Bank staff that contributed to this Report, especially the staff of the Research and Monetary Policy Department, as well as the participants. Thank you.