Governor Murat Çetinkaya's Speech at the Briefing on Inflation Report 2016-III (Ankara, 26/07/2016)

Distinguished Guests,

Welcome to the briefing held to convey the main messages of the July 2016 Inflation Report.

Before commencing my speech, I would like to tell that our hearts are filled with grief over those martyred in the heinous attacks against our nation, express my condolences to the families of the victims, and wish speedy recovery to those wounded. We strongly believe that no horrendous act can damage our bold efforts towards development. I would like to reiterate that we, the Central Bank of the Republic of Turkey, will continue to put all our efforts together for the welfare of our country.

The report typically summarizes the economic outlook underlying monetary policy decisions, shares our evaluations on macroeconomic developments and presents our medium-term inflation forecasts, which were revised in view of the developments in the last quarter, along with our monetary policy stance. Moreover, at the end, I would like to talk about our evaluations on the recent steps taken by our Bank.

In addition to the main text, the Report includes six boxes entailing up-to-date and interesting analyses on various topics. There are boxes in this Report that analyze the importance of food prices in the fight against inflation, discuss how developments in the tourism industry affected the current account balance, growth and employment, and look into the effects of minimum wage hikes on the job market. In addition, the report includes boxes that elaborate on the welfare effect of shortened completion times of public investments, analyze the correlation among firm size, the variety of imported goods, the import ratio in expenditures on intermediary goods and firms’ position as exporters, and scrutinize the relationship between monetary policy and loan and deposit rates. The titles of the boxes are shown on the slide. All of these analyses shed light on important and current issues pertaining to the Turkish economy. I strongly recommend that you read these boxes, which will soon be published on our website.

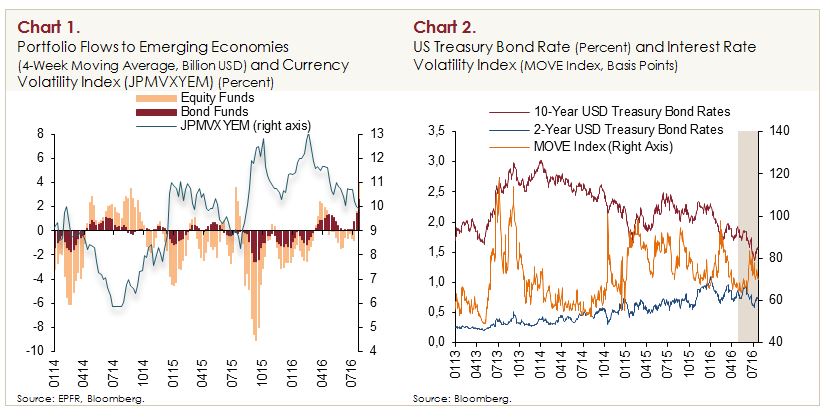

I would like to commence my speech by reviewing the global economic outlook, given its ongoing influence on our policies. As you all know, changing expectations over the monetary policies across advanced economies and the Brexit referendum that resulted in UK’s decision to leave the European Union were the key drivers of global market volatility in the second quarter of 2016. Global uncertainties and the sluggish growth across emerging economies triggered portfolio outflows from emerging markets, particularly in equity funds (Chart 1). Global growth expectations were revised downward after the Brexit referendum, spurring hopes that major central banks would deliver additional support for the markets if necessary, and the growing sentiment that the Fed would postpone the rate hike until next year boosted the global risk appetite.

Prospects of a prolonged period of low policy rates across advanced economies helped bring global volatility indices down again, causing long-term interest rates to plunge (Chart 2). In fact, the US 10-year bond yields slid to an all-time low in July, sinking below the mid-2012 bottom. More recently, long-term interest rates in advanced economies have fallen to historic lows, thereby driving portfolio flows into emerging market bonds. Accordingly, market rates have been declining across emerging economies. Additionally, as oil prices recover and the Brexit referendum is expected to affect growth and trade in mostly advanced economies, the partially improved sentiment towards oil-exporting emerging economies has supported financial conditions in emerging economies. In this regard, the emerging market exchange rate volatility index also declined.

Global uncertainties also spilled over into the Turkish economy in the second quarter; yet, the favorable course of macroeconomic indicators besides the new measures we adopted in line with the road map of August 2015 as well as the monetary policy simplification helped to tame the uncertainty and risk sentiment over Turkey. Consumer inflation was broadly in line with our forecasts of the April Inflation Report in the second quarter of 2016, while underlying core inflation continued to improve on the back of services prices. In this period, again in line with our April Inflation Report projections, the current account deficit continued to narrow, and the economy remained on a moderate and steady growth track. The CBRT maintained its policy stance, which is tight against the inflation outlook, stabilizing for the foreign exchange liquidity and supportive of financial stability, and took further steps towards monetary policy simplification. Accordingly, risk premiums and market rates began falling in the second quarter, while inflation expectations dropped, and the Turkish lira appreciated in real terms.

The mid-July market fluctuations led by domestic developments resulted in market volatility and a renewed increase in risk premiums. Against this background, we announced new measures on July 17 to ensure the smooth operation of markets. These measures help financial system to have efficient access to liquidity. We closely monitor market depth and pricings, and thus, if necessary, will take all measures required to maintain financial stability. We believe that the recovered global risk appetite and the measures taken will render the spillovers from domestic uncertainty short-lived and limited. I would also like to remind you that the implementation of the planned structural reforms will boost the growth potential and favorably affect the perceptions regarding the Turkish economy.

1. Monetary Policy and Financial Conditions

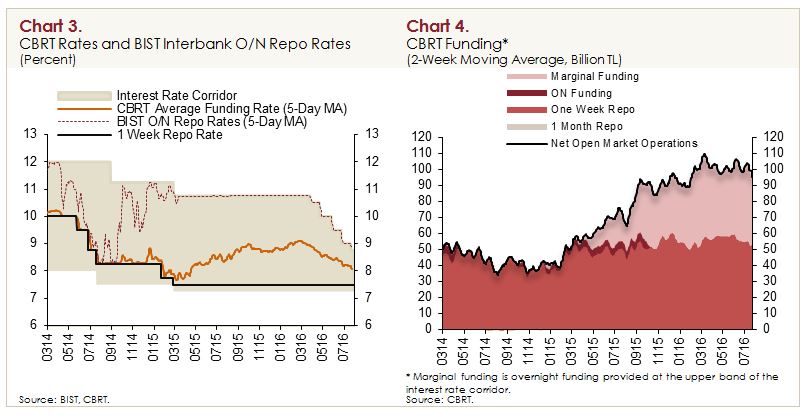

We maintained the tight liquidity policy stance in the second quarter of 2016 on account of inflation expectations, the pricing behavior and other factors affecting inflation. Waning global volatilities, the favorable course of core inflation indicators and the effective use of policy tools we described in the road map helped us continue with monetary policy simplification. In addition, the liquidity measures we adopted on July 17 put a lid on the domestically induced market turmoil. To this end, we lowered the marginal funding rate to 8.75 percent after two 50 basis points cuts in May and June followed by a 25 basis points cut in July. On the other hand, we kept the one-week repo auction rate and the overnight borrowing rate unchanged at 7.5 and 7.25 percent, respectively (Chart 3).

One-week repo auctions continued to be the main tool for the CBRT funding, while the share of the marginal funding remained flat (Chart 4). The weighted average funding rate receded to around 8.2 percent in July. Interbank overnight repo rates dropped in line with the reductions in the upper band of the interest rate corridor. I would like to underline that our monetary policy stance will remain dependent on the inflation outlook in the upcoming period.

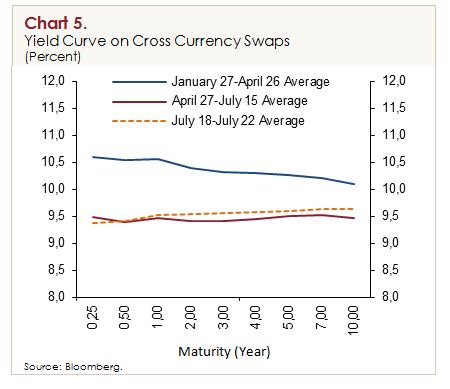

Amid continued monetary easing across central banks of advanced economies, improving macroeconomic indicators for Turkey and monetary simplification, the yield curve shifted downwards in all maturities until mid-July compared to the previous reporting period, as shown on the slide (Chart 5). However, in the subsequent days, some of the gains from the yield curve were lost partially due to domestic uncertainty.

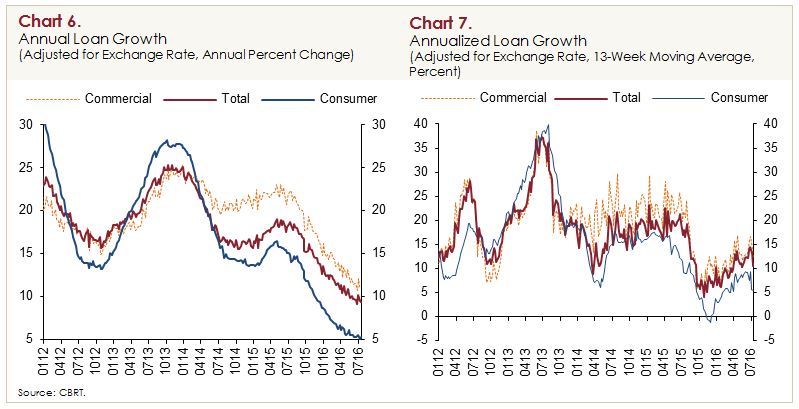

The annual growth rate of loans extended to the non-financial sector fell to 9.5 percent in the second quarter of 2016 (Chart 6). In this period, commercial loans continued to post a higher grow rate than consumer loans as they have since the start of 2014. These developments in loan growth and composition continue to support the re-balancing process and financial stability. The annualized growth rates in 13-week moving averages show that both commercial and consumer loans have picked up since early 2016 (Chart 7). Yet, this recovery is mostly prompted by seasonal effects as growth rates are still below the previous year’s averages. We expect that the adjustments to risk weights of consumer loans, wage developments and improved financial conditions may support loan growth in the upcoming period.

In terms of the economic fundamentals, fragilities were mostly contained by the tight monetary policy, the improvement in the current account balance, macroprudential measures, reasonable loan growth and favorable loan composition for price stability and financial stability. Sustaining fiscal discipline was also a major factor enhancing the resilience of our economy in this period. It is important to restrict the repercussions from recent domestic and external developments on financial markets and the economy. Therefore, we believe that the ongoing effective implementation of the measures laid out in the road map and the sustained tight monetary stance have alleviated the economy’s sensitivity to global shocks, thus supporting financial stability. We closely monitor market developments and will continue to take additional steps to support financial stability if necessary.

2. Macroeconomic Developments and Main Assumptions

Now, I will talk about the macroeconomic outlook and our assumptions on which our forecasts are based. First, I will summarize the recent inflation developments, and then continue with the domestic and external demand outlook upon which we based our projections.

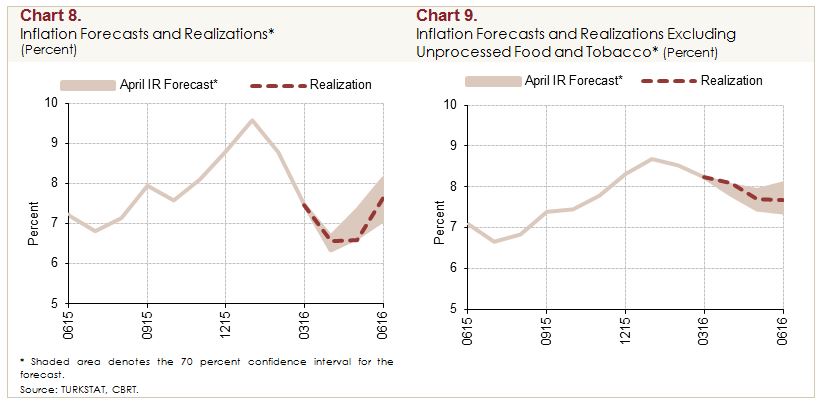

In the second quarter of 2016, consumer inflation edged up by 0.18 points quarter-on-quarter and hit 7.64 percent, remaining broadly in line with the April Inflation Report forecast (Chart 8). The rise in inflation was mostly attributed to unprocessed food prices and energy prices, whereas annual inflation across core goods and services, which constitute core inflation, was down. Thus, inflation excluding unprocessed food and tobacco prices declined as predicted in the April Inflation Report (Chart 9). As cumulative exchange rate effects on annual inflation have been fading, import prices, particularly for oil, have been soaring. Therefore, inflation was up in food and energy but down across core items in the second quarter.

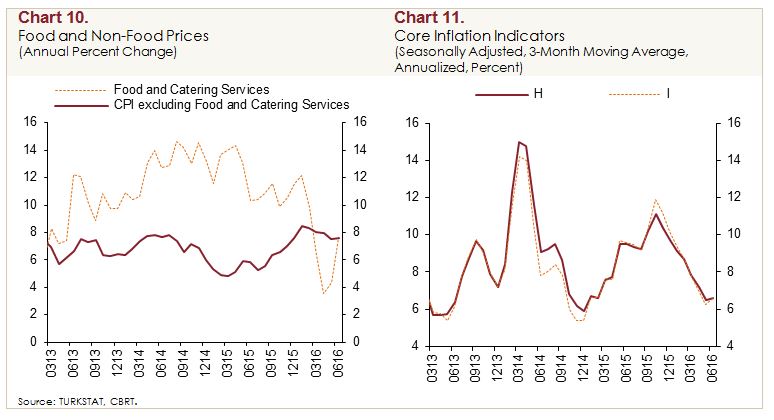

The first quarter’s modest outlook for unprocessed food prices deteriorated slightly in the second quarter. Although price hikes in catering services have recently been slow, changes in food prices brought annual food and catering services inflation up to 7.65 percent in the second quarter (Chart 10). Meanwhile, annual inflation excluding food and catering services remained on a steady decline.

The underlying services inflation slowed down in the second quarter. This was largely owed to price movements across services such as accommodation, transport and catering driven by the developments in the tourism industry. On the other hand, despite waning cumulative exchange rate effects, the underlying core goods inflation remained broadly unchanged from the previous quarter as the depreciation of the Turkish lira in May passed through to particularly prices of durable goods. Accordingly, the underlying core inflation indicators continued to slow thanks to prices of services (Chart 11). In sum, the food and energy-driven increase in inflation was partially offset by the second-quarter improvement in core items.

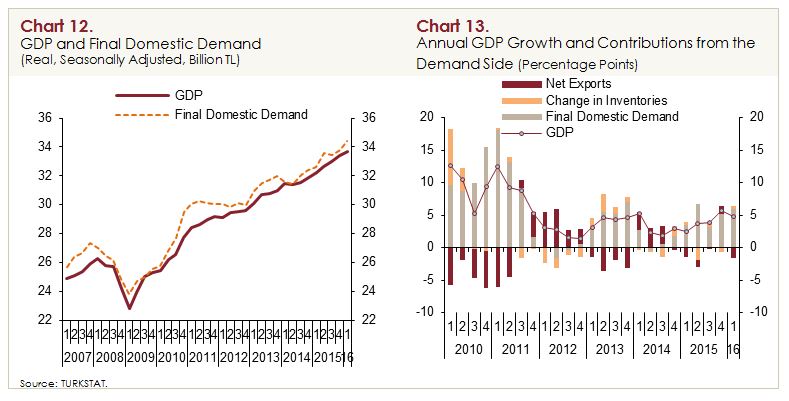

Our key message on the real economy will be that economic activity remains on a moderate and steady growth track. In the first quarter of 2016, GDP expanded by 0.8 and 4.8 percent in quarterly and annual terms, respectively, in line with the outlook presented in the April Inflation Report (Chart 12). On the spending front, final domestic demand was the main driver of annual growth as expected, whereas net exports contributed negatively to growth (Chart 13). The contribution of final domestic demand to growth has been through consumption spending in this period.

Current indicators for the second quarter of 2016 point to a mild economic activity. Industrial production posted a 0.4 percent decline from the previous quarter’s average in the April-May period. Domestic demand indicators for sales, production and imports also hint at some quarterly increase for the second quarter, but suggest that this increase might be smaller than the one in the first quarter. In addition, external trade data for April-May period indicate that foreign demand may make a subdued contribution to growth.

We predict that growth will be stimulated largely by domestic demand throughout 2016. Notwithstanding substantial wage hikes, the favorable course of employment will continue to support consumption via the income channel. We expect private investments to edge up in the second half of 2016 on the back of domestic demand conditions and the modest global growth. Yet, domestic demand growth will be spurred mostly by increased consumption spending. We believe that the anticipated recovery across our export markets will continue to support exports in the remainder of the year. On the other hand, the developments in the tourism sector constitute some downside risk to economic activity and the current account balance.

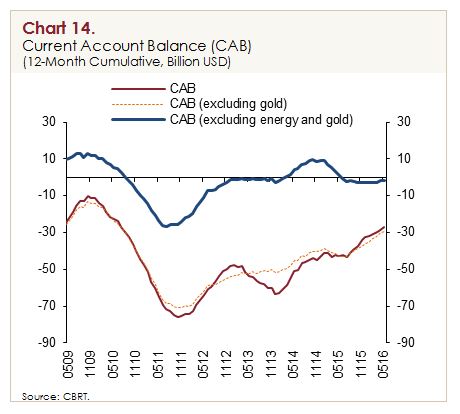

In sum, domestic demand is likely to increase owing mainly to consumption spending and external demand will recover amid the expected mild growth in our export markets in 2016. Despite this outlook on demand composition, we expect the current account balance to improve further in 2016 thanks to the ongoing macroprudential measures and the low course of commodity prices (Chart 14).

Esteemed Guests,

As you all know, food, energy and import prices also play a great role in inflation forecasts. Therefore, before moving on to forecasts, I will briefly talk about our assumptions regarding these variables.

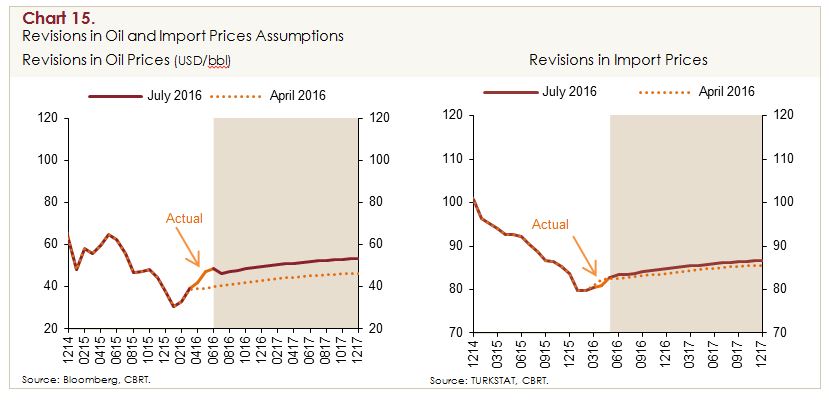

Oil and import prices edged up in the inter-reporting period. Thus, we revised our assumptions both for crude oil prices and USD-denominated import prices upwards compared to April Inflation Report (Charts 15). With regard to annual averages, we increased the crude oil price assumption from 40 USD to 44 USD for 2016. Also, we revised the assumptions for annual percentage changes in average import prices upwards by 0.6 points for 2016.

Now, I would like to talk about our assumptions regarding food prices. Food inflation saw a marked decline due to unprocessed food prices in the first quarter, yet this was reversed in the second quarter. However, food inflation path in June proved close to April Inflation Report projections. The recent upside movements in unprocessed food prices will cause food inflation to surge in July, while a downside correction in food prices is likely in the period ahead. We expect food price inflation to be lower than the previous reporting period at end-2016 on account of the measures taken by the Food and Agricultural Products Markets Monitoring and Evaluation Committee (the Food Committee) and the seasonal decline in food demand owing to tourism. Accordingly, we revised the assumption for food price inflation downwards from 9 percent to 8 percent for 2016, and kept it unchanged at 8 percent for 2017.

Medium-term forecasts are based on an outlook that adjustments to taxes and administered prices will be consistent with the inflation target and automatic pricing mechanisms. The medium-term fiscal policy stance depends on the MTP projections covering the 2016-2018 period. We closely monitor the effects of the minimum wage rise in early 2016 on producer costs, aggregate demand and inflation. Despite a limited lump sum tax rise through tax adjustments in tobacco products in July, we saw that firms opted for a high-rated price adjustment amid rising costs.

3. Inflation and the Monetary Policy Outlook

Esteemed Guests,

Now, I would like to present our inflation and output gap forecasts based on the outlook I have described so far.

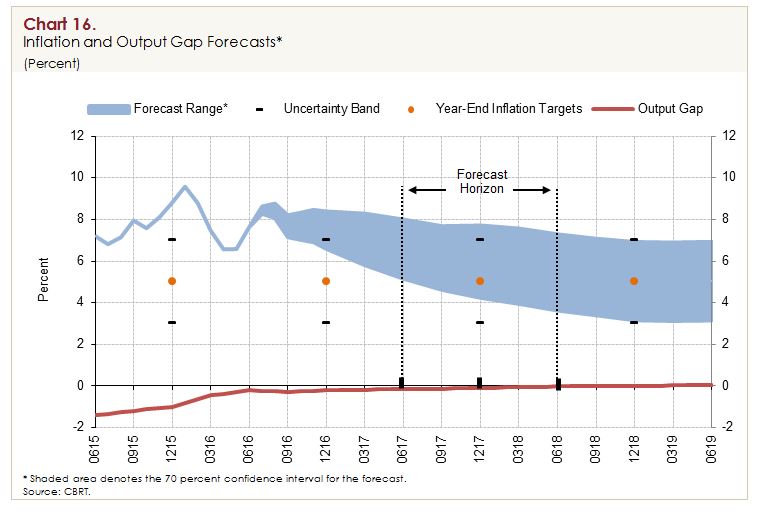

In view of the above economic conditions I have mentioned here and our policy stance and assumptions, we kept our inflation forecasts for the upcoming period unchanged since the previous Report. Given a decisive policy stance that focuses on bringing inflation down, inflation is estimated to converge gradually to the 5-percent target. Accordingly, inflation is likely to stabilize around 5 percent as of 2018 after falling to 7.5 percent in 2016 and to 6 percent in 2017. Accordingly, inflation is expected to be, with 70 percent probability, between 6.6 percent and 8.4 percent (with a mid-point of 7.5 percent) at end-2016 and between 4.3 percent and 7.7 percent (with a mid-point of 6 percent) at end-2017 (Chart 16).

The Turkish lira followed a fluctuating course following the April Inflation Report, while oil prices inched up and import prices remained close to April Inflation Report projections. Although we estimate that TL-denominated import prices will be higher than the previous reporting period, the pass-through to inflation will be restricted depending on the moderate course of domestic demand in the second half of the year. The recent upward movements in unprocessed food prices and adjustments in tobacco prices will push inflation remarkably upwards in July. Meanwhile, we project that food prices will see a downward correction in the upcoming period. In addition, core inflation is likely to hover more modestly across the year compared to the previous reporting period. We envisage that the rise in tobacco prices is expected to push the end-2016 inflation forecast upwards compared to the April projections, yet the improvement in headline inflation trend and the developments in economic activity are believed to compensate for this increase. Against this background, we kept year-end consumer inflation forecasts for 2016 and 2017 unchanged.

In addition to these forecasts, we summarize a variety of risk assessments regarding the overall macroeconomic outlook and the monetary policy in the Risks and Monetary Policy section of the Inflation Report. You can examine the Report for details.

Esteemed Guests,

In the final part of my speech, I would like to share some information on some developments I mentioned in the April Briefing, which was the first Briefing on the Inflation Report under my governorship.

One of the issues I emphasized in the April Briefing was that permanent price stability would only be achieved through joint efforts. Secondly, I underlined the role of structural factors in the higher-than-targeted and volatile course of inflation. In this context, I told that we would be willing to work on these issues in detail and fight with inflation also on the structural front by raising public awareness and acting in coordination with relevant parties.

Accordingly, efforts of the Food Committee to keep food price increases at reasonable rates and eliminate price volatilities to contribute to price stability continued in this period. In this scope, concrete policy proposals were produced by product basis, the prices of which create notable volatility in the producer price index. Regarding this, items with high weight in inflation were given priority. Among these concrete measures, endeavors related to red meat stood out. Particularly, measures taken by the Ministry of Food, Agriculture and Livestock supported domestic supply and contributed to a relatively milder course in red meat prices.

Efforts undertaken by the Food Committee do not only consist of product-based activities. In addition to market monitoring and evaluation activities, structural issues like licensed warehousing, specialized commodity exchanges, agricultural subsidies, producer organizations and data collection and compilation are also handled. For example, revision of the Wholesale Market Law in accordance with this is also under construction.

As a result, efforts undertaken by the Food Committee constitute valuable examples of joint efforts to achieve long-lasting price stability. Rendering these acquisitions permanent, deepening these efforts and focusing also on structural issues, thereby pulling food-related inflation down to levels consistent with consumer inflation target are of great significance.

Secondly, I would like to talk about our efforts to investigate structural issues. Taking concrete steps towards interinstitutional coordination in structural issues will offer important achievements regarding inflation. With a view to preparing the infrastructure to this, “Structural Economic Research“ Unit was established under the CBRT and studies were initiated to develop joint solution offers on structural issues on the agenda with relevant institutions. We expect the studies undertaken by this unit on price rigidities and market disorders in Turkey to play a guiding role by creating a joint discussion platform.

I would like to mention another step towards a better understanding of these structural factors. Efforts to enhance institutional infrastructure to compile regional information on corporate sector developments and the pricing behavior have gained momentum. The results to be obtained are intended to serve as inputs to the Monetary Policy Committee. Accordingly, we attempt to enhance the communication network between the Central Bank and the corporate sector.

The Central Bank has been paying regular visits to corporate sector firms in various cities in our country. Through these visits, managers and specialists of our Bank report the cyclical evaluations regarding the firms’ activities and expectations on the one hand, and deliberating towards detecting structural problems on a sectoral basis, on the other. We are accumulating an undeniably valuable source of information through this channel as well. Sharing this information with policymakers and the public is also in our agenda.

In the new period, we foresee important changes regarding our communication policy with the relevant parties as well. We have recently published a press release. In the upcoming period:

- Technical talks will be held with investors and analysts.

- Regular meetings will be held with investors in financial centers abroad;

- Meetings will be held to facilitate exchange of views with industrial and trade chambers and other corporate sector representatives;

- Periodic meetings will be held with the representatives of the press agencies and the economic media;

- Monthly meetings currently held with banks’ economists will be held when deemed necessary depending on the declining need following new practices;

- Briefings on inflation reports and other communication practices will be sustained.

In addition to all these endeavors, we took some steps towards the simplification of the monetary policy as well. As I mentioned at the start of my speech, our recent monetary policy decisions should be evaluated within the simplification process. Our ultimate goal through simplification is to achieve a narrow and symmetrical corridor and provide funding via a single rate. The CBRT funding is currently made through two separate channels, which is a challenge against the communication of our monetary policy stance. In this context, we took steps like (i) interest rate adjustments towards narrowing the interest rate corridor, (ii) balanced allocation of daily quantity auction amounts to enhance the predictability of the TL liquidity policy and (iii) deliberations to improve the efficiency and foreseeability of the Turkish lira liquidity management.

We hold the view that simplification will contribute to the efficiency of the transmission mechanism. Therefore, we are aiming at terminating the simplification process in the monetary policy at a reasonable point of time. However, the timing and pace of this termination will eventually depend on the developments affecting inflation and financial stability.

Esteemed Guests,

While concluding my remarks, I would like to thank all my colleagues who contributed to the Report, primarily those at the Research and Monetary Policy Department as well as the members of the Monetary Policy Committee. I also thank every one of you for your participation and patience.